The High Cost of the Unknown: The Invisible Threat: Why Critical Metals Supply Chain Opacity is Costing OEMs Billions

In the high-stakes race toward electrification, the western automotive industry has hit a wall. It isn't a lack of technology or consumer demand, but rather a lack of transparency. While manufacturers have spent decades perfecting just-in-time production, the raw materials powering the EV revolution, lithium, cobalt, nickel, and rare earth elements, remain hidden behind a thick fog of multi-tier uncertainty.

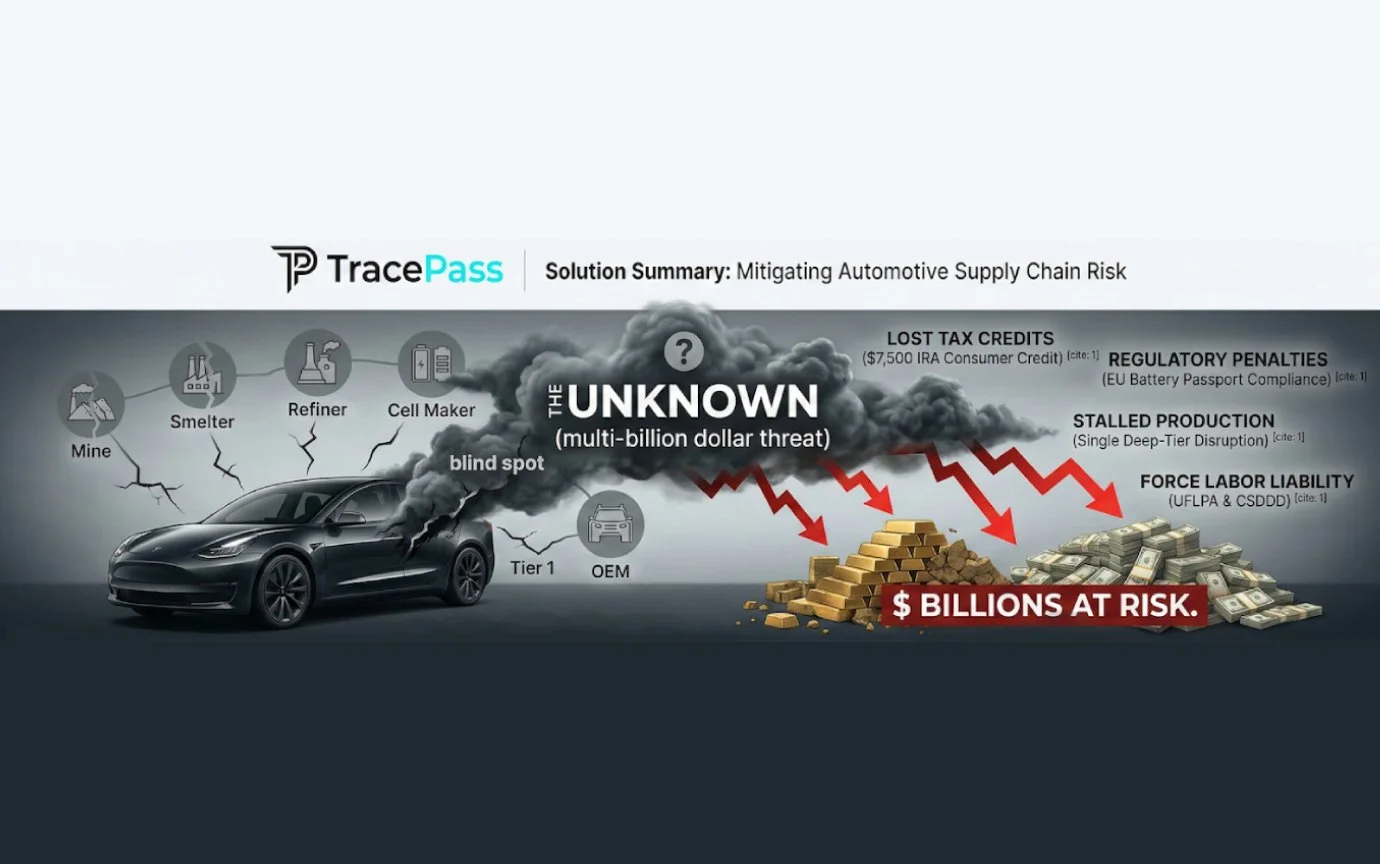

This opacity is much more than a logistical headache. It is an invisible threat that is already costing the industry billions in stalled production, heavy regulatory penalties, and lost tax incentives.

The Tier 1 Illusion and the Deep-Tier Reality

Most automotive companies maintain strong, transparent relationships with their Tier 1 suppliers. However, research into the cobalt supply chain reveals a sobering reality: most Tier 1 partners are up to six tiers removed from the actual mining and extraction level.

This visibility gap creates a domino effect of financial risk. Just last year, major OEMs were forced to temporarily halt production at key assembly plants due to sudden shortages of rare earth magnets. These components are essential for electric power steering and audio systems, yet they were caught in a supply chain squeeze several tiers down the line. With China currently refining the vast majority of the world’s rare earths, any export curb ripples through the market instantly. Without true traceability, OEMs are effectively blind to these shocks until the assembly line literally stops.

The High Price of Non-Compliance: IRA and EU Regulations

In the modern regulatory landscape, opacity equals insolvency. The rules of the game have changed, and "we didn't know" is no longer a valid legal defense.

The $7,500 Tax Credit Wall Under the U.S. Inflation Reduction Act (IRA), vehicles are only eligible for consumer tax credits if their critical minerals are sourced from the U.S. or free-trade partners. By 2027, this requirement jumps to 80%. Without verifiable, granular data on the origin of every gram of lithium, OEMs lose the competitive edge of these subsidies. This effectively prices their vehicles out of the mass market.

The EU Battery Passport Starting in early 2027, every EV battery sold in Europe must have a Digital Battery Passport. This isn't just a simple label. It is a full digital audit trail of carbon footprint, recycled content, and ethical sourcing.

The Forced Labor Liability Regulations like the UFLPA in the US and the CSDDD in the EU place the entire burden of proof on the manufacturer. If a sub-tier supplier is flagged for human rights violations in regions like the DRC, entire shipments can be seized at the border. The costs include legal fees, storage, and permanent damage to brand equity.

TracePass: Turning Transparency into a Competitive Asset

At TracePass, we believe that what you can’t see will eventually hurt you. The days of relying on self-disclosures and manual spreadsheets are over. To survive the next decade, automotive leaders must move from reactive crisis management to proactive supply chain intelligence.

The bottom line is simple. Supply chain opacity is no longer just a "sustainability" or "marketing" issue. It is a core financial risk. The billion-dollar question for western OEMs is no longer if they can build EVs, but if they can prove how they built them.

Is your supply chain a strategic asset or a billion-dollar liability?

References & Further Reading

U.S. Department of Energy: Critical Minerals Assessment 2025/2026

European Commission: Circular Economy and the Battery Passport Regulations

The Inflation Reduction Act: Understanding Mineral Sourcing Requirements

PwC: 2026 Automotive Trends and Supply Chain Resilience Report

Reuters: Supply Chain Disruptions and the Hidden Tiers of EV Production